The Dollar Wrecking Ball: Why is a strong US dollar so dangerous?

The rising US dollar strength is starting to produce cracks across economies and markets.

Blackrock operates a portfolio management platform called Aladdin, which is used by some of the largest institutions in the world (Microsoft, Met Life, Credit Suisse etc.) The Coinbase partnership, exclusive only to Bitcoin, will let Blackrock’s institutional clients access crypto trading, custody, prime brokerage and reporting via Coinbase Prime, whilst using Aladdin for risk and portfolio management.

The partnership is just another in a long series of headlines announcing more institutional entry into the crypto markets. In March, Goldman Sachs did its first ever over-the-counter Bitcoin transaction with Galaxy Digital. In April, Fidelity, which manages retirement savings (401(k)) as one of its core businesses, will let its customers allocate up to 20% of their savings to Bitcoin. Headlines clearly indicate growing interest, but institutional floodgates have yet to fully open.

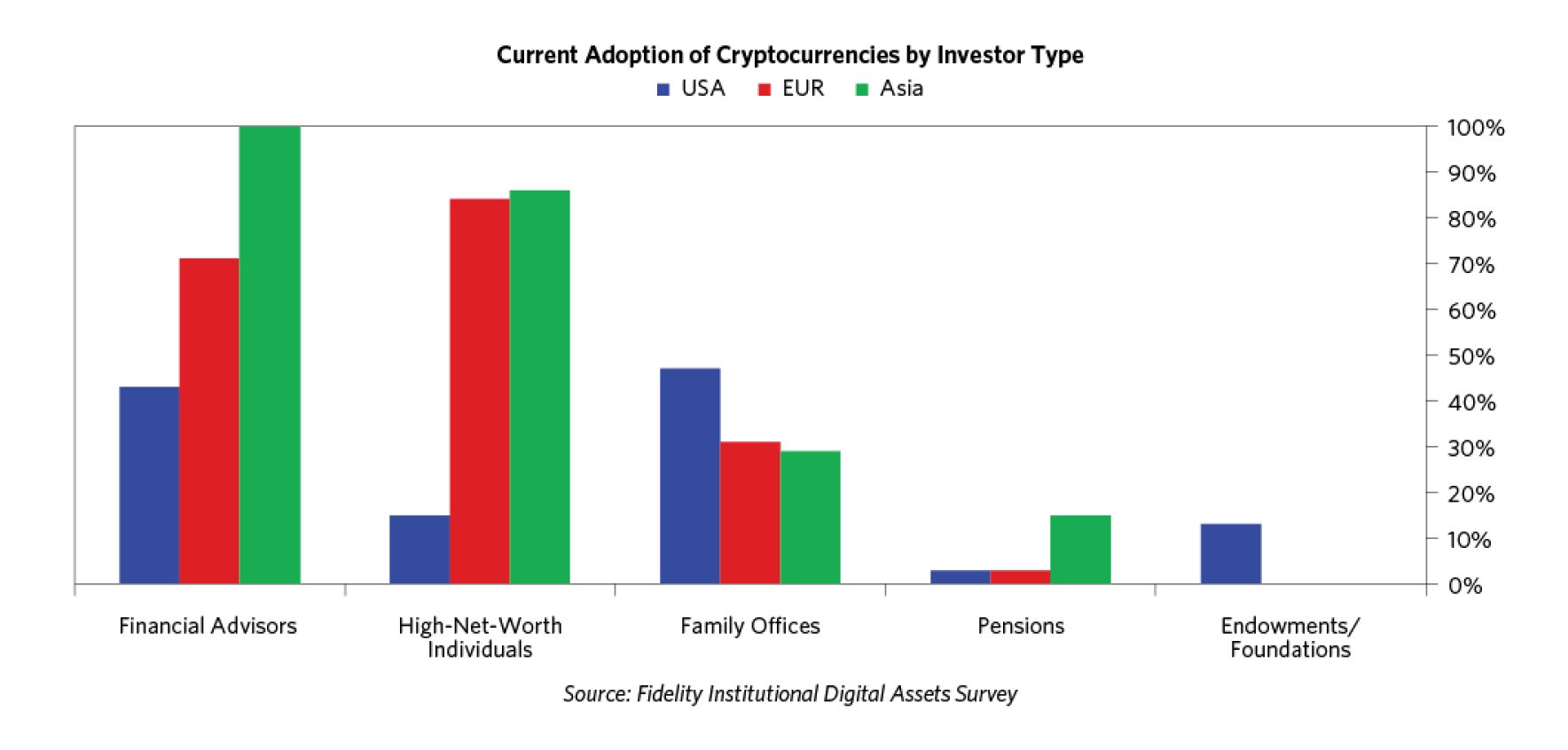

Estimates show that institutions hold around 1 million BTC, which amounts to approximately 5% of the available supply. If history is to serve as a guide, then we can expect this number to shoot up significantly. We have already seen a significant uptick in interest toward purchasing digital assets. The report shows that 8 out of 10 institutions are considering buying cryptocurrency. In the graph below is the distribution of institution allocation into digital assets:

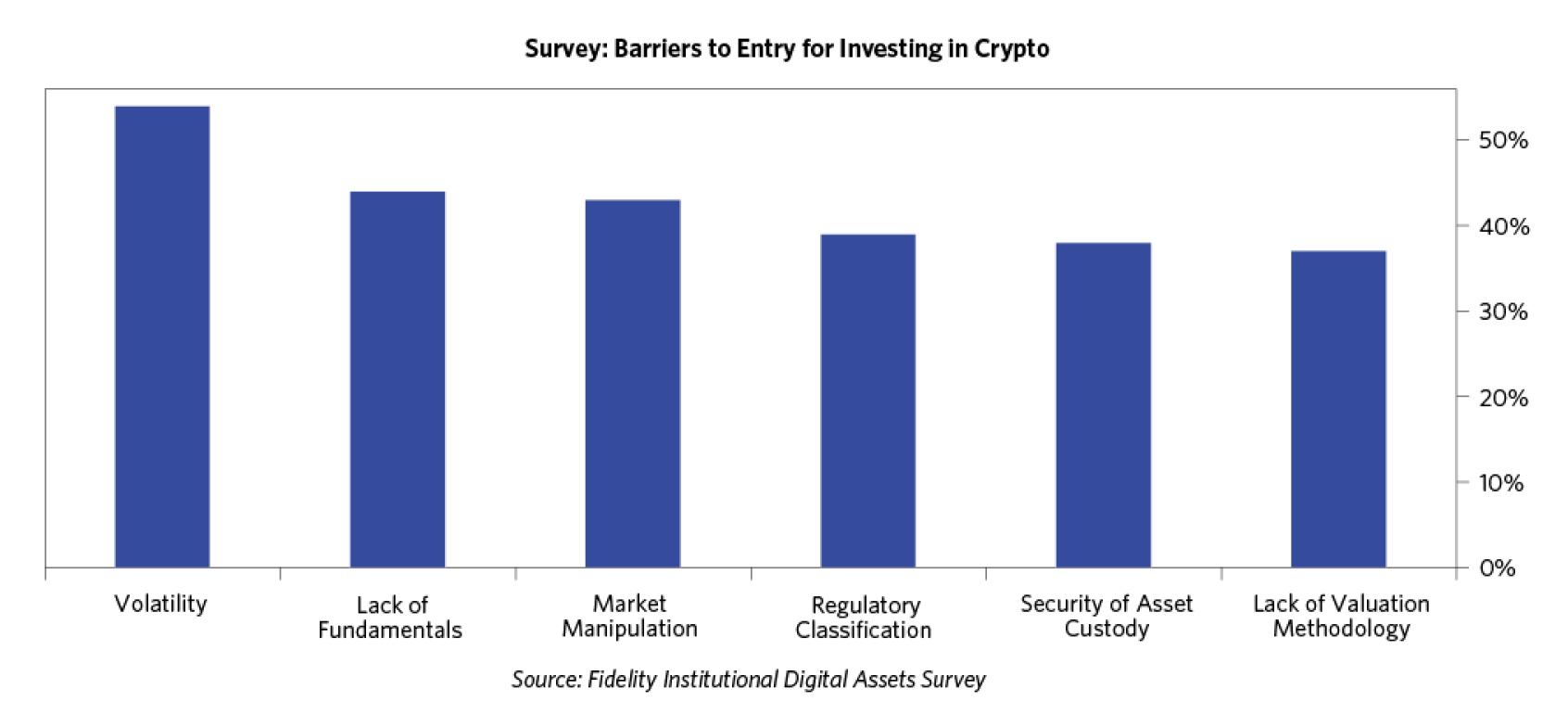

We can see that the least allocated are the more regulated institutions (pension funds, mutual funds, sovereign wealth funds etc.). They must adhere to a very rigid set of rules, which has not yet allowed them to dip their toes. Here is a list of the most cited problems regarding entry into the digital space:

Some of these problems stem from the nature of the asset class, like its volatility or difficulty of valuing assets. Although, many point to the fact that as adoption grows, cryptocurrencies will stabilize and lower their volatility. The other problems are more structural and are being gradually worked on. Let’s delve a little deeper into the main structural obstacles which keep institutions out.

Insufficient liquidity

The crypto market capitalization at $1 trillion is minuscule compared to the US stock market or the US bond market (both at around $125 trillion). Bridgewater estimated Bitcoin liquidity at 1.4% of the US stock market liquidity, thus amounting to a relatively small allocation in their portfolios. Institutions trade in a large size, which means they require enough liquidity so that the market can readily process any of their transactions. It takes time to build a sufficiently large liquidity pool for institutions to invest in, and a vast majority of cryptocurrencies still do not represent a viable option. Only Bitcoin and Ethereum are now large enough for institutions to include them in their portfolio.

However, we can expect a few other cryptocurrencies to grow big enough to become institutional material. The development of indexing, ETFs and derivatives will also help widen exposure to relatively smaller projects.

Complex trading and investing strategies, risk management

As we saw in the table above, volatility is cited as the main problem for most institutions. Pension funds, managing retirements or mutual funds in charge of billion-dollar accounts cannot afford an 80% drawdown during bear markets. Excessive volatility is cryptocurrency’s natural problem and cannot be solved by adjusting the structure of the crypto markets. However, institutions are apparently finding a way to participate regardless of volatility as their client increasingly demand allocation into the digital space. And as their share gets more significant, volatility is likely to subdue.

Institutions also deploy capital in a much more complex way than a traditional retail investor. For institutions to put on their strategies, they not only need liquidity but also require a wide variety of hedging tools, risk management tools and derivatives. When an institution opens a trade in a traditional security, they can construct a sophisticated strategy involving options, futures and ETFs, which allow them to precisely determine the amount of risk they are taking. Digital assets are limited in this sense, though they are quickly evolving. Some cryptocurrencies already offer futures and options; hence these tokens see the most institutional adoption. One pressing problem is a lack of a US spot Bitcoin ETF which would be backed by the actual cryptocurrency. Counterparts in Europe and Canada have already successfully released spot ETFs. These passive products are highly popular in traditional markets. They tend to be very transparent (solving regulatory issues), highly liquid and offered at low fees. Institutions can access some spot Bitcoin tools in over-the-counter markets, but they still lack proper custodial management.

These problems are, however, being gradually solved. Higher adoption and larger market capitalization will help create a wider variety of derivatives. A number of funds are already in the works of releasing a bitcoin spot ETF. The question is now only when the SEC decides to let these funds come through. There are also companies trying to create an index similar to S&P500, which would be essentially tracking the wider crypto market. Cryptex.finance developed a token (TCAP) which does just that.

Custody, compliance and regulation

Compared to retail investors, institutions need to comply with strict and rigid rules, which aim to keep investors’ funds safe whilst in the hands of a third party. Cryptocurrencies still lack a clear regulatory framework, making institutions reluctant to enter the space. First and foremost, institutions must know whether their funds are stored in a safe manner. Proper custody in cold storage is an absolute must, and there already is a variety of companies working to solve this issue (Copper, BitGo, Gemini, Coinbase custody etc.).

Another major problem is KYC (know your customer) and AML (anti-money laundering) regulations. Crypto anonymity principles are unfortunately not acceptable for larger institutions. Even this issue is, however, actively being solved so that both institutions and retail stay satisfied. Aave, for instance, created a separate branch called Aave Arc, where every participant is KYC and AML compliant. Even the liquidity pools are separated from the regular pools. Another example is Compound, a Defi project which created a gateway called Compound treasury, separated from the main protocol and AML and KYC compliant.

So as you can see, there are still hurdles to overcome before the floodgates fully open. However, once they do, the amount of incoming money inflow is incomparable to retail.

So, what does this money inflow mean for prices?

Hard to imagine anything but pushing prices higher. The available research clearly shows the rapid pace of innovation, higher adoption than during the internet era, rising interest from retail and institutions, and just an overall positive sentiment. If we put these factors together and merge them with 101 Economics of supply and demand, it is difficult to see how this space would be shrinking. It is likely that institutional flows will be one of the main demand drivers in the next bull cycle.

It is also important to note that as the institutional presence becomes a norm, it might alter the behaviour of cryptocurrencies as an asset class. As we mentioned earlier, institutions have strict rules regarding their investment strategies. They will most likely consider cryptocurrencies not as an antidote to traditional markets but rather as its new volatile component. Cryptocurrencies are long-duration assets, most similar to growth stocks (stocks which don’t yet have significant (or any) revenue, but investors bet on the firm’s potential to grow), which are considered risky assets. These assets strive in an environment of a growing economy, low interest rates and plentiful liquidity; the exact opposite of the current environment. We have already seen cryptocurrencies mimic the behaviour of growth stocks (correlation with the tech-heavy NASDAQ is very high), and we can expect this behaviour to continue going forward, probably even amplify. It does not seem likely that investors would rush into cryptocurrencies whenever there is stress in the markets, just as we have seen in recent months.

We can expect institutional investment to continue growing

Considering the absolutely dominant return offered by digital assets, coupled with immense innovation and adoption, it would be quite illogical for institutions not to participate. We expect the trend of “adoption headlines” to continue as the market keeps growing and evolving into a major asset class. The growing adoption will then consequently help the sector to consolidate and become more accessible to everyone around the planet. It is hard to imagine how we are all not going to own at least some crypto in the future.

The rising US dollar strength is starting to produce cracks across economies and markets.

A chance at disrupting and replacing the prevalent corporate structure.

The most recent crypto bull market resulted in some NFTs receiving an impressively high price tag.

A pivotal lawsuit is nearing its end; it is crucial to know what it could mean for crypto.

Komentáre

Ak si prajete pridať komentár, musíte byť prihlásený.